{kind=link}

More and more people are turning to technology to help them make positive strides in getting better ways to access care and benefit from simpler healthcare experience.

This upsurge in consumer demand for digital-based health services is creating a new model for care in which patients and machines are joining doctors as part of the healthcare delivery team, according to results of a survey from Accenture.

The Meet Today’s Healthcare Team: Patients + Doctors + Machines report surveyed almost 8,000 people across seven countries to assess the rates of adoption for health-related technology and people’s attitudes towards sharing electronic health records (EHRs).

Unsurprisingly, the adoption rate for health-related technology is increasing across the board with the exception of health-related website use which seems relatively steady. Technologies, ranging from mobile apps to smart scales to wearables have seen significant growth in the past few years with no sign that this growth will slow.

And wearables are not simply ways to gather data and to monitor health.

Wearables also encourage healthy behaviours through subtle nudges such as a vibration to remind you to move after periods of inactivity or gamification and competition on data-sharing sites. Some products can even warn of impending cardiac arrest.

The survey found that the number of people willing to share EHRs is also increasing. However, there is a clear preference towards sharing data with a doctor, medical practitioner or family member whereas sharing data with their employer or a government agency was treated with more suspicion. Use of wearables in the workplace to monitor employee efficiency may further heighten this suspicion.

Artificial Intelligence (AI) – which offers significant benefits for both the wearer and the healthcare provider – seemed to split respondents with just under half expressing a positive view of the benefits of AI when it came to interpreting their EHRs.

For insurers, the report highlights two trends of particular interest: the growth of wearable technology rising from 9% in 2014 to 33% in 2018 and the high numbers of respondents willing to share their data with a health insurance provider (72%).

Both trends indicate a growing opportunity for wider integration of technology and wearables with the health insurance which should benefit both the consumer and the insurance provider.

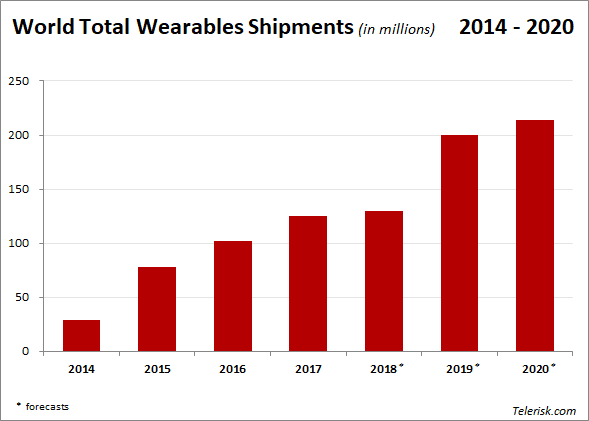

Since the first iterations of wearables in the early 2000s, which were little more than electronic versions of old-fashioned pedometers, the market has exploded.

An estimated 125.5 million devices were shipped in 2017 with forecasts that the market could almost double to 240 million devices by 2021.

This growth of wearables has overlapped significantly with developments in smart watch technology making products like the Apple Watch one of the best-sellers in this category.

Other products are broadening the range of what we would consider health-related wearable. Spire produces a breathing-monitoring device that helps manage stress and Neuroon is an eye mask that promises to improve your sleep. Some firms are even promising clothes with built-in sensors.

The senior “Gold Rush”

Contrary to the assumption that this kind of tech is for younger and active users; a growing selection of wearable products are specifically aimed at seniors.

These ranges from more traditional products which gather and monitor health data to shoes equipped with sensors that sound an alarm if someone falls or check that wearer has moved recently. In these cases, wearables are not only providing healthcare benefits but also quality of life benefits for seniors with increased, or sustained, mobility and independence.

And these products aimed at those aged 55 may be the next area of explosive growth. The trillion dollars market for senior-focussed products is being described as a “gold rush”.

This growth of products aimed at the lucrative seniors’ market would likely lead to even wider adoption of these technologies by the under 55s. Biohackers, for example, are always looking for ways to repurpose medical technology to gain an edge. In turn, these innovations are often what spark wider consumer adoption creating a cycle of adoption and innovation.

With wide adoption of external, surgically implanted external blood glucose sensors and recent FDA (Food and Drug Administration) approval for blood glucose implants in the US, implants are likely to be the next iteration of these advancements. One clinical study described the widespread adoption these as imminent: “perhaps even in the next decade.”

Opportunities for health insurers

In addition to investments in the technology aspects of this market, the growing overlap of technology and healthcare has attracted the attention of the health insurance market.

A recent CapGemini report forecasts that “wearables will impact all parts of the insurance customer journey” through personalized products, continuous underwriting, policyholder service & risk control and claims management.

Some of these ideas are not new and traditional insurers saw the benefits of wearables relatively early. Early partnerships with firms such as Fitbit offered incentives and discounts based on the user’s level of activity.

However, the effectiveness and benefits of these initiatives are unclear as the data collected was minimal and often shared via the employer, something users were reluctant to do as Accenture found.

However, with thousands of healthtech startups and devices producing significantly richer sets of EHR data, there are growing opportunities to integrate wearables into health insurance.

Mountain View, California’s HealthIQ is offering fitness-oriented individuals more favourable insurance plans due to their active and therefore assumedly healthier lifestyles. HealthIQ surveyed over a million people and partnered with medical researchers to support this approach and had over $8 billion in coverage under management in May 2018.

Other startups are offering to coordinate data management between the insurance firm and the user, cutting the employer out of the picture. Australia’s Fitsense is placing itself in the centre of this relationship by providing data analysis and processing to help build individual risk profiles on consumers for use by insurance and healthcare providers.

With such innovations and opportunities, the increasing use of EHRs gathered through wearables by health insurers is set to increase. This offers opportunities for both the consumer with targeted customized coverage, and insurers who can better manage their risks.

However, with insurers potentially holding massive troves of what amounts to users most personal information, the onus will be on insurers and data handling services to protect and manage this data carefully.

A data loss, or worse a data compromise, would significantly erode the confidence of users and likely stifle this opportunity for integration.